February 18, 2021

Daily Position Report

Market Focus

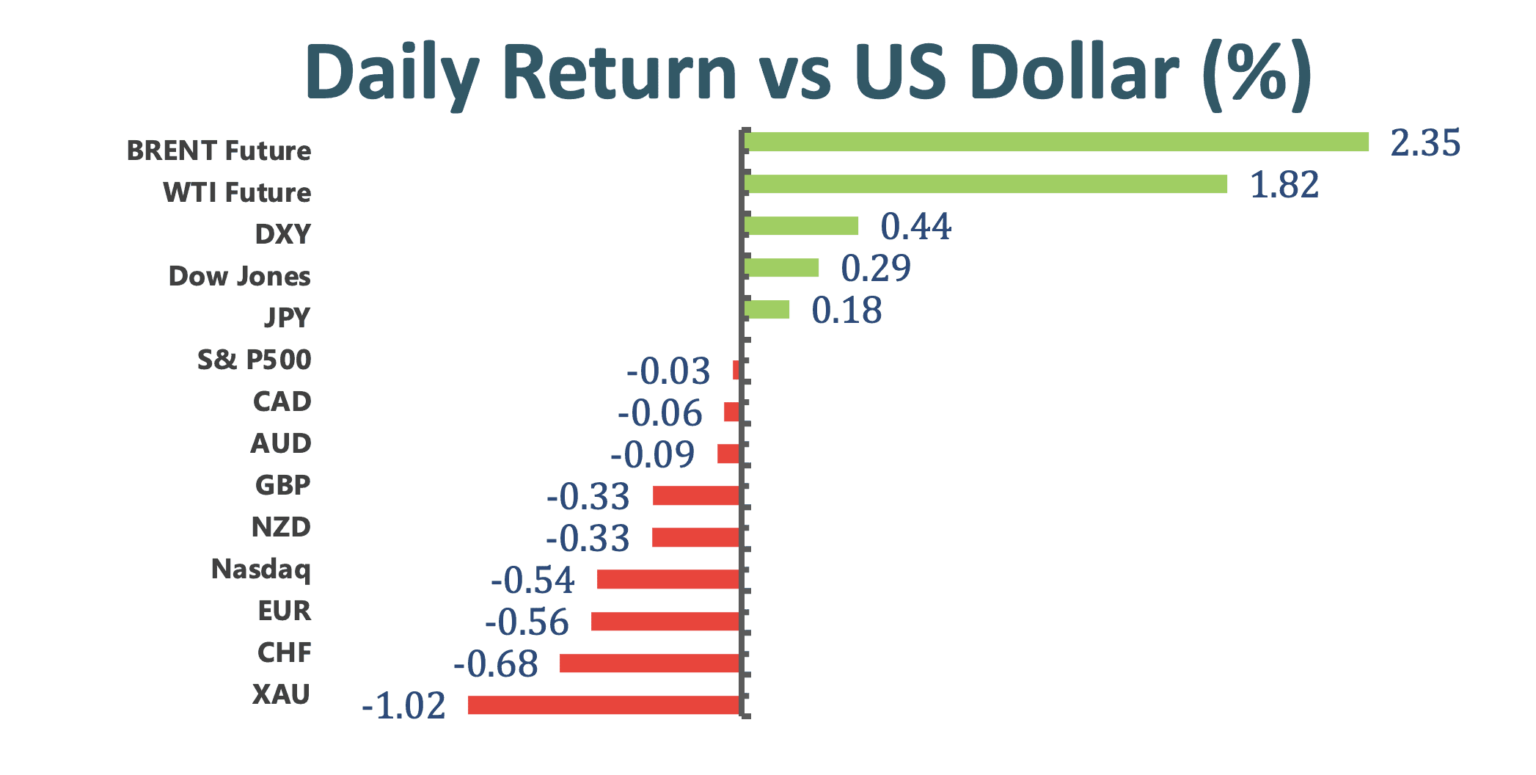

US equity market dropped on a second day amid rising long term treasury yield, the US 10-year treasury yield hit as high as 1.33% prior to some pullbacks. Technology stocks lead the decline, with the Nasdaq Composite Index retreated 0.54% from high. Meanwhile, energy stocks like Devon Energy Corp. and Chevron Corp. hiked albeit Texans were hit by power outage, blackouts are expected to last until at least Thursday.

US retail sales accelerated in the month of January, increased by 5.3% from last December. The recovery in the retail segment is an encouraging signal that consumers are actually spending their stimulus checks on physical goods instead of putting it into saving accounts.

UK Prime Minister Boris Johnson announced on Wednesday that they are planning to ease the recent lockdowns on February 22nd, stating “the unwinding of restrictions will be done in stages”.

The cryptocurrency mania resumes with Bitcoin refreshing record high, jumped beyond $52,000 on Wednesday. The digital token recently gained tremendous traction after Tesla Inc. announced its $1.5 billion purchase. JPMorgan Chase & Co. strategists said Bitcoin’s volatility needs to ease to prevent its rally from fizzling.

Key takeaways from FOMC January meeting minutes:

• The committee thinks it will be “some time” before it achieves the substantial further progress needed for tapering.

• The board will not be bothered by a rise in prices later this year, given vaccines and pent-up demand.

• Economy is far from achieving its goal of maximum employment.

• FOMC saw inflation risks as more balanced, most still viewed the risks as weighted to the downside.

Market Wrap

Main Pairs Movement

Gold fell to the lowest level in more than two months as US 10-yield treasury yield topped 1.3%, and dollar index rebounded to 91. The precious metal headed for a fifth straight decline on Wednesday, and is currently struggling to penetrate $1774 support line. The upbeat retail sales prompted demand for the US greenback, putting pressure on Gold.

The euro fell 0.54% against the US dollar, closed around 1.2041, the lowest price in two weeks. European restrictive measures will persist under spreading UK new variants, capping any upward move in the shared currency. Meanwhile, Italian Prime Minister Mario Draghi says EU needs common budget to combat recessions.

The Cable dropped 0.3% albeit upbeat CPI figure. The annual CPI increased by 0.1% from last year’s 0.6%, printed 0.7% compared to forecast of 0.6%. PM Johnson’s plan to lift lockdown help to alleviate some of Sterling’s pressure.

Commodity linked Aussie and Kiwi declined 0.1% and 0.4% respectively. Aussie has been outperforming Kiwi since Feb 4th, AUDNZD rallied 2.06% throughout this period. The uptrend would continue since RBA will likely maintain its current dovish tone until inflation and unemployment targets are achieved unless there is a downside surprise in Australian job data.

Technical Analysis:

EURUSD (Daily Chart)

Euro dollar is drifting away from the short-term descending trendline towards 1.193 support level. The pair will first encounter a longer term upward trendline which was eking out a long bullish run during the last eight-month. A breakthrough from the downside will mark the end of Euro’s bullish trend against the safe-haven greenback. However, the road to south will be bumpy as it has to take down multiple critical supports such as the 1.2 handle and previous stern resistance of 1.193. Conversely, bidders will have to overcome the blue descending trendline in order to regain meaningful upward momentum. MACD on the daily chart shows tendency of a bearish reversal.

Resistance: 1.206, 1.217, 1.2333

Support: 1.193, 1.163

GBPUSD (Daily Chart)

Cable retreated from yearly highs as price kissed the ceiling of an upward tunnel. Cable managed to stand above 1.38 hurdle dated back to March 2018, but the overbought RSI signal helped to pull the overextended price down toward 1.38. If this support fails to defend further decline, then DMA50 will still be supportive in the downside. Nonetheless we maintain our long-term bullish bias on this pair given its strong fundamental, and most of the previous Brexit negativity have been removed from the market. MACD on the daily favors the bulls.

Resistance: 1.416, 1.4625

Support: 1.38, 1.338, 1.2769

XAUUSD (Daily Chart)

Gold’s value continues to deteriorate in the wake of dollar strengths and higher US long bond yield. Gold was previously stuck within support band between $1838 and $1823, and it failed to stand on top of previous neckline, which speculators usually perceive as a strong sell signal. Price then dipped to November’s low of $1770, but not quite reached 50% Fibonacci support level around $1765. The bearish bias will remain intact in the long term, but given the magnitude of plummet in the past five trading days, we expect the bears to take a breather during the rest of this week. It seems like MACD on the daily chart changes its tone from a bullish reversal to continuation of bearish trend.

Resistance: 1823, 1872, 1930

Support: 1765, 1691

Economic Data

|

Currency

|

Data

|

Time (TP)

|

Forecast

|

|

AUD

|

Employment Change (Jan)

|

08:30

|

40K

|

|

EUR

|

ECB Publishes Account of Monetary Policy Meeting

|

20:30

|

|

|

USD

|

Building Permits (Jan)

|

21:30

|

1.678M

|

|

USD

|

Initial Jobless Claims

|

21:30

|

765K

|

|

USD

|

Philadelphia Fed Manufacturing Index (Feb)

|

21:30

|

20.0

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|