December 15, 2021

Market Focus

US stock declined on Tuesday amid downbeat market sentiment, as pressures increased on the Federal Reserve to tighten monetary conditions in a faster than expected pace. The headline US Producer Price Index (PPI) released on Tuesday rose at an annual pace of 9.6% in November, which is more than market’s expectation of 9.2%. The surging US PPI and CPI data weighed on the equity market as investors worried that this could make the Fed to act more aggressively, despite the officials have give no signs that they would rush up to tighten monetary policy. On top of that, concerns about the spread of new Omicron variant still remained as the UK reported one death related to the newly discovered variant. Investors now await the critical Federal Reserve monetary policy decision on Wednesday, which might provide some clues on the pace of bond tapering and interest rate hikes.

The benchmarks, S&P 500, Nasdaq 100 and the Dow Jones Industrial Average both dropped on Tuesday amid downbeat market mood and a perspective that relief that Fed is about to end the cycle of easy money. S&P 500 was down 0.7% on a daily basis and the Dow Jones Industrial Average declined with a 0.3% loss for the day. Ten out of eleven sectors stayed in negative territory as the information technology and real estate sectors are the worst performing among all groups, losing 1.64% and 1.27%, respectively. The Nasdaq 100 dropped the most with 1.0% loss on Tuesday and the VIX rose almost 12%, as investors started to move their investments from stocks to other asset.

In Asia, China will release Industrial Output for November and retail sales data, which are expected to show slower economic activity due to a real-estate recession and falling consumption. Meanwhile, Chinese property developer shares and bonds plunged to the lowest since early 2017.

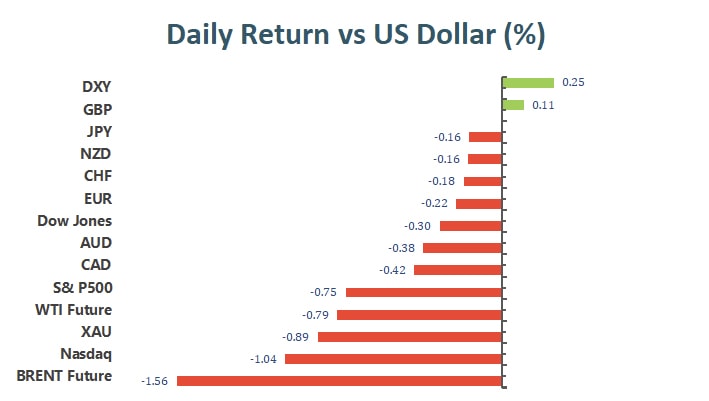

Main Pairs Movement:

The US dollar advanced on Tuesday , staying in positive territory amid risk-off market sentiment. The DXY index dropped to a daily low under 96.15 in mid-European session, but then started to see heavy buying and rebounded towards 96.5 level. The higher yields and weaker stocks both lend support to the greenback, which rose 0.21% on a daily basis. Investors now expect the Fed to tighten its monetary policies in a faster pace due to higher PPI and CPI data.

GBP/USD advanced 0.10% on Tuesday amid upbeat UK jod data, as the number of people claiming unemployment-related benefits declined by 49.8K in November. The cable touched a daily top in late European session, then retreated back to surrender some of its intraday’s gain. Meanwhile, EUR/USD dropped to a weekly low under 1.126 area, losing 0.21% for the day.

Gold slipped and touched a daily low around $1766 amid renewed US dollar strength. The falling US stock market failed to pushed the precious metal higher, which dropped 0.87% on a daily basis. Meanwhile, WTI oil tumbled 1.16% for the day, as more countries reimpose restrictions to avoid an Omicron variant outbreak. The rising Covid-19 cases and the downbeat market mood both acted as a headwind for the black gold.

Technical Analysis:

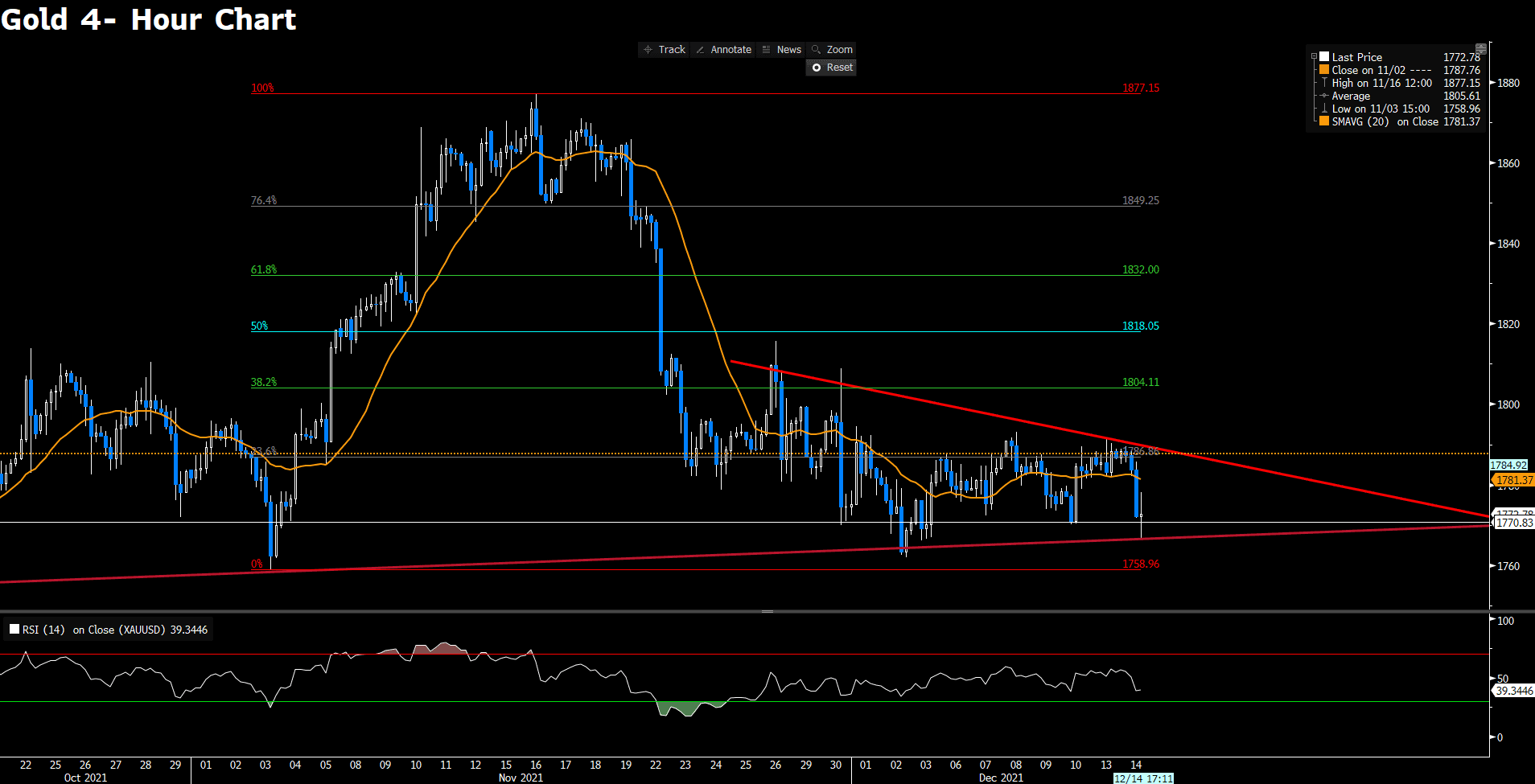

XAUUSD (4- Hour Chart)

The precious metal, gold, slipped to fresh daily low below 1780 after the annual PPI surged to 9.6% in November. The sell- off mainly came from the market’s reaction as a high inflation might quicken the pace of the US Fed’s QE taper as well as hikes in the interest rates. From the technical perspective, gold continues to trade in a subdued manner within 1786- 1770 ranges. In the near term, the outlook of gold looks bearish as it trades below the 20 SMA, and heading to test its support at 1770. For now, any further rallies below 1770 will confirm a sell as if gold penetrates the level, it will at the same time break the descending wedge. More price action is likely to be in place after Wednesday’s FOMC policy announcement.

Resistance: 1786, 1804, 1818

Support: 1770, 1758

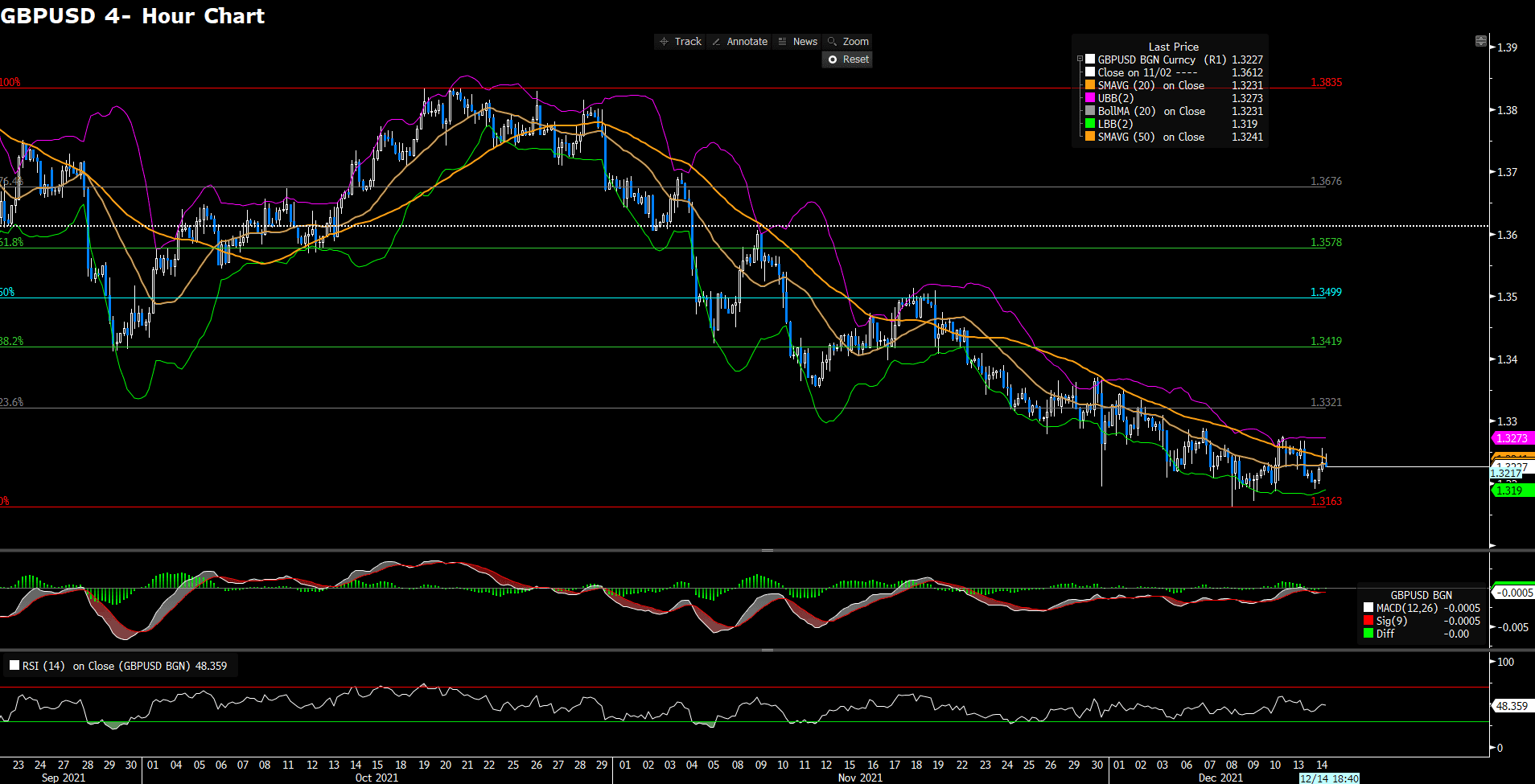

GBPUSD (4- Hour Chart)

GBPUSD stays in the positive territory neat 1.3230 on Tuesday as the US dollar has a difficult time to find the demand after the release of PPI report. However, the pound’s demand is at the same time at stake as the Omicron infections in the UK looks worse than expected. As a result, further price action eyes on Wednesday’s FOMC announcement. From the technical aspect, despite the recent rebound, the outlook of the currency pair continues to remain bearish as it still trades below the 20 and 50 SMAs on the four- hour chart. In the meantime, the RSI is neither in the oversold nor overbought territory, punctuating the lack of upside strength. On the upside, GBPUSD needs to at least trade above the SMAs to reclaim bullish momentum in the near- term. Trading above the resistance at 1.3321 will re- confirm a bearish- to- bullish trend.

Resistance: 1.3321, 1.3419, 1.3499

Support: 1.3163

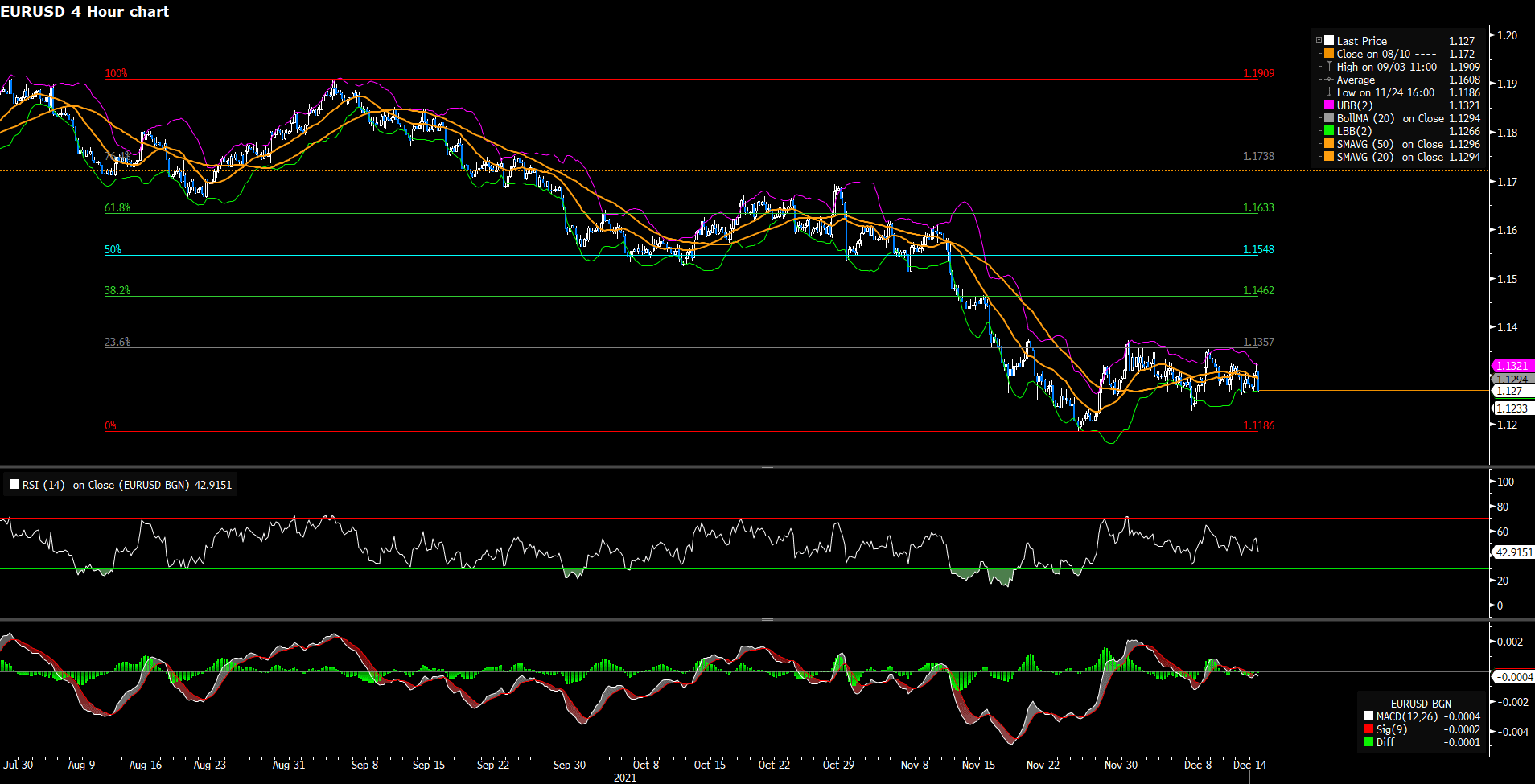

EURUSD (4- Hour Chart)

EURUSD trades near its weekly low at 1.1269 amid the advances in the US government bond yields. The focus remains on Wednesday’s US Fed decision and Tuesday’s the ECB meeting. From the technical analysis, EURUSD continues to seesaw within 1.1233- 1.1357 range. On the four- hour chart, the outlook remains bearish as the pair continues to trade below the 20 and 50 Simple Moving Averages; in the meantime, it trades within the lower bounce of Bollinger Band. The RSI indicator remains neutral, suggesting a directionless situation. On the upside, EURUSD needs to trade above 1.1357 in order to begin another bullish trend; the pair might extend further gain p to 1.1462 if it successfully breaches the immediate resistance at 1.1357.

Resistance: 1.1357, 1.1462, 1.1548

Support: 1.1186

Economic Data

|

Currency

|

Data

|

Time (GMT + 8)

|

Forecast

|

|

NZD

|

RBNZ Gov Orr Speaks

|

03:00

|

N/A

|

|

CNY

|

Industrial Production (YoY) (Nov)

|

10:00

|

3.6%

|

|

GBP

|

CPI (YoY) (Nov)

|

15:00

|

4.7%

|

|

USD

|

Core Retail Sales (MoM) (Nov)

|

21:30

|

0.9%

|

|

USD

|

Retail Sales (MoM) (Nov)

|

21:30

|

0.8%

|

|

CAD

|

Core CPI (MoM) (Nov)

|

21:30

|

N/A

|

|

USD

|

Crude Oil Inventories

|

23:30

|

-2.600M

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|