January 16, 2022

Market Focus

The broad U.S. equity market close the week mixed. The Dow Jones Industrial Average retreated 0.56% to close at 35911.81, the S&P 500 gained 0.8% to close at 4662.85, and the Nasdaq composite gained 0.59% to close at 14893.75. This week marks the beginning of earnings season, as companies release Q4 results from 2021. Goldman Sachs and Bank of America are among the bigger companies that will be releasing earning results this week, then followed by Netflix and Procter and Gamble. The benchmark U.S. 10 year treasury yield remains at 1.793%, while the 30 year treasury yield sits at 2.127%.

On this week’s economic docket, China’s GDP figures, Britain’s CPI and unemployment data, the Eurozone’s CPI data, and U.S. Initial Jobless claims figures are due for release. The U.S. equity markets will be closed on Monday, due to Dr. Martin Luther King’s day.

Main Pairs Movement:

The Dollar Index rose 0.32% over the course of Friday’s trading. The Dollar rose amid weaker than expected retail sales figures. Market participants may have interpreted the weak retail sales figure as a signal to a weaker U.S. economic environment, however with imminent rate hikes on the horizon and continuously rising bond yield’s the Dollar seems unstoppable.

Cable lost 0.23% over the course of Friday’s trading. Britain’s better than expected quarterly GDP growth did not provide enough upward momentum for the Pound, but Cable ended the week with a solid 0.71% gain.

The Euro-Dollar pair retreated 0.35% over the course of Friday’s trading. The ECB’s president failed to provide any fuel to the recovery of the Euro.

Gold also faltered against the Dollar on Friday. The precious metal lost 0.27% against the Dollar.

Technical Analysis:

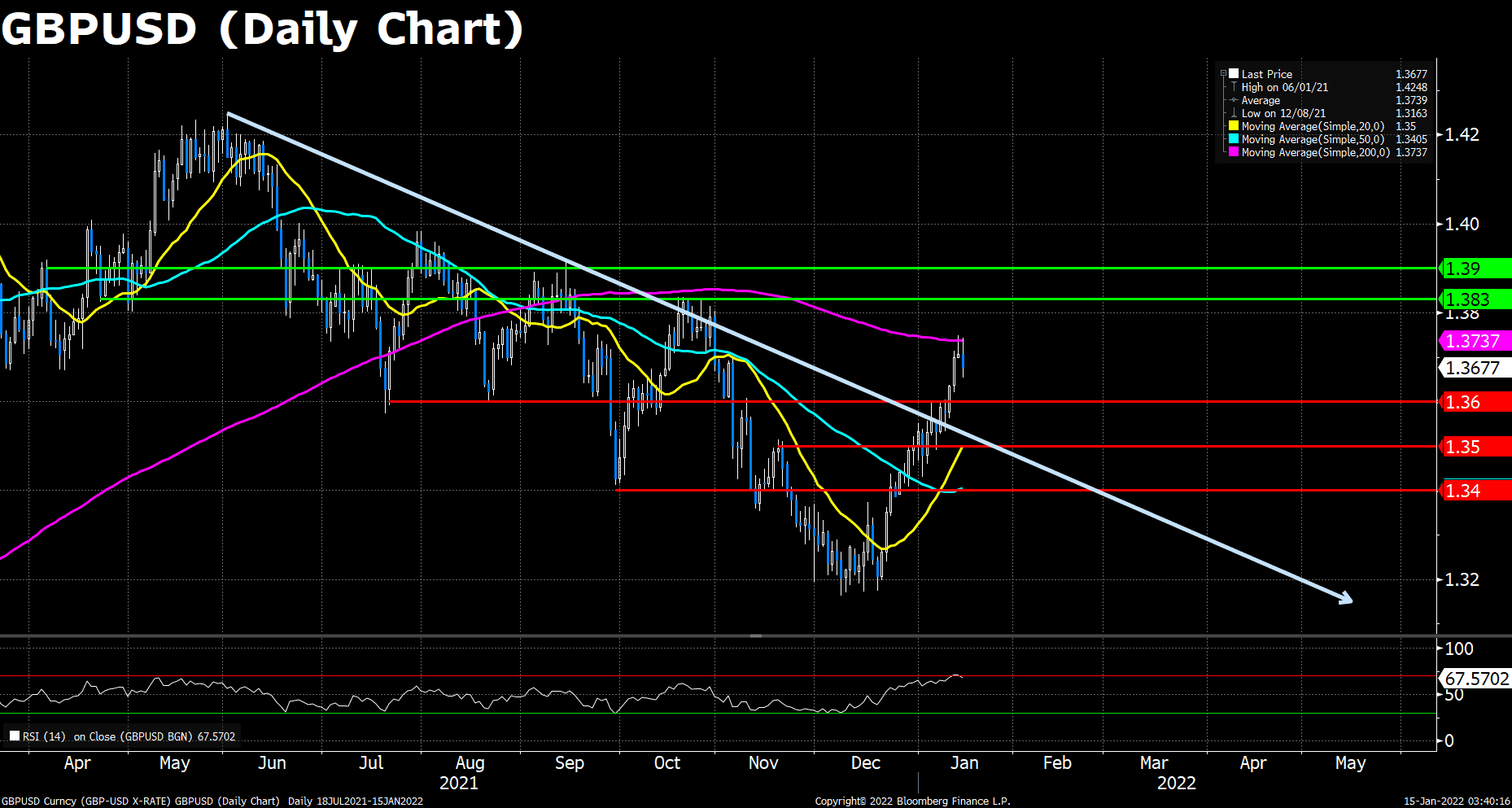

GBPUSD (Daily Chart)

On Friday, a pack of solid UK macroeconomic data failed to underpin the British pound, which struggled to cling to the 1.3700 figure, falling during the New York session. At the time of writing, the GBP/USD is trading at 1.3675. It is worth noting that the US Dollar Index reclaimed the 95.00 level, up some 0.25%, sitting at 95.05, underpinned by the rise of the US 10-year T-bond yield, up to 1.75%, a three basis points gain. Moreover, the dismal sentiment in the equity markets revived the demand for safe haven assets, which is also in favor of the greenback.

On the technical front, after being rejected by the persistent 200 DMA resistance, Cable keep falling during Friday’s trading, heading to the next support line at 1.3600. The RSI for the pair reads 67.44, dropped out from the overbought territory, but not necessarily will the pair bounced back as the dollar starts to price in the effect of the rate hike announcements by Fed.

Resistance: 1.3737 (200 DMA), 1.3830, 1.3900

Support: 1.3600, 1.3500, 1.3400

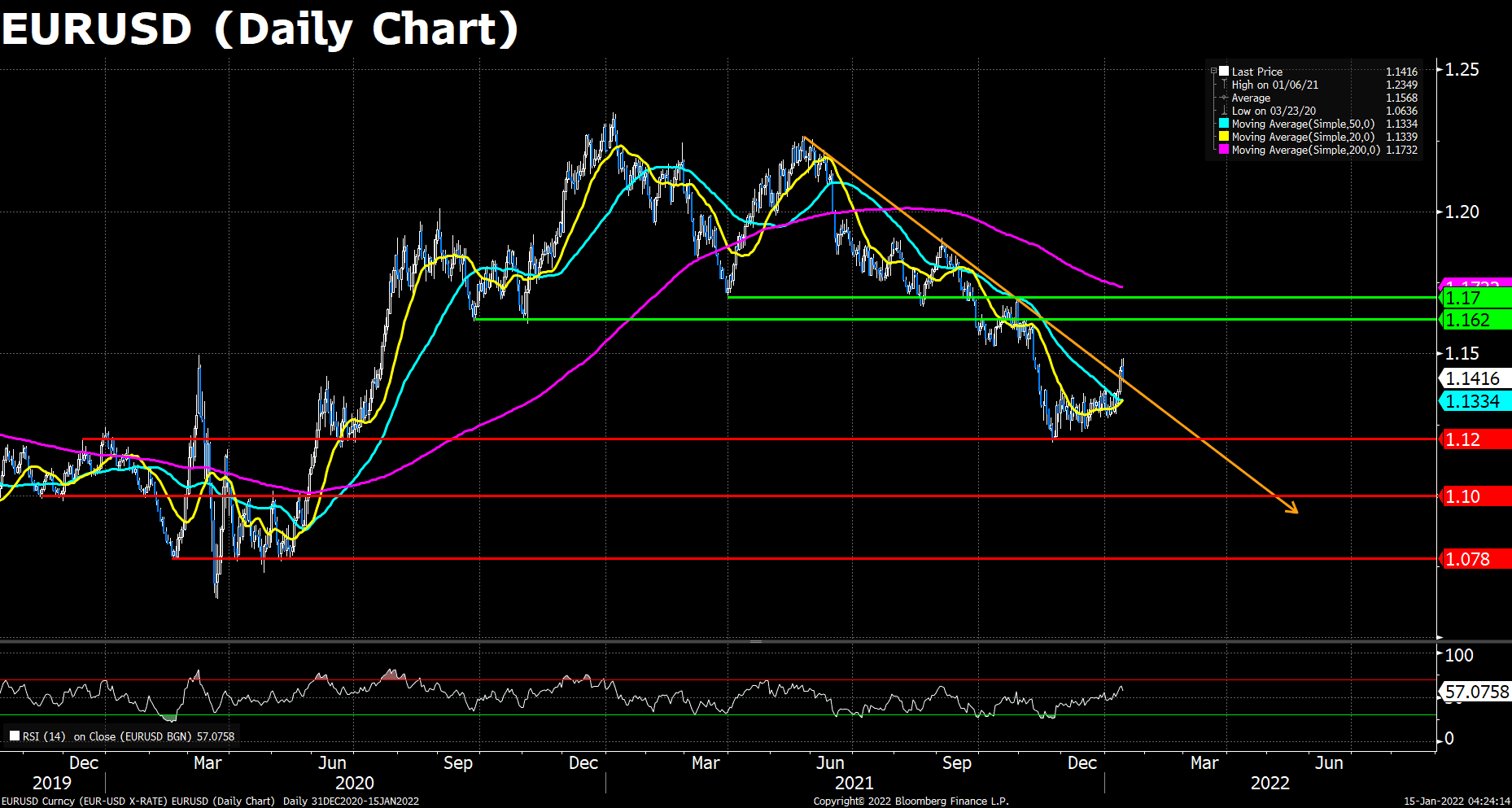

EURUSD (Daily Chart)

The Euro selling has continued into the North American session, though the bearish intra-day momentum has for the moment eased with the pair finding support above the psychologically important 1.1400 figure. At current levels around the 1.1415 mark, the pair is trading lower by about 0.4% and is over 0.6% lower versus its month highs in the 1.1480s. Apparently, the downbeat US data released on Friday didn’t scare of the dollar bulls, as they bet the Fed will focus more on the elevating inflation and the tight labour market, rather than a monthly Retails Sales or a non-deadly Omicron spread.

On the technical, Euro bears once tested the 1.1400 support but was rejected. The pair lingers around 1.1415 at the moment, and as the dollar strengthened, the downside risk increased. The RSI for EUR/USD has dropped from the 60s, suggesting the upside traction is diminishing. As previously mentioned, If the pair managed to cling on the 1.1400 threshold at the end of the week, then we could expected the pair to reach the next resistance level at 1.620; however, if failed, the looming Fed’s hawish monetary policies may push the dollar up, again dragging the Euro pair to the downside.

Resistance: 1.1620, 1.1700

Support: 1.1200, 1.1000, 1.0780

XAUUSD (Daily Chart)

Gold slipped for the second-consecutive day amid dismal US economic data revealed on Friday. XAU/USD closed the day at $1,818 a troy ounce. During the New York trading hours, Gold failed to capitalize on negative readings on US Retail Sales and Industrial Production, and disappointing Consumer Sentiment. In the meantime, the US 10-year benchmark yield advances firmly five basis points, sitting at 1.771%, heading to the weekly highs around 1.80%.

As to technical, market sentiments toward the yellow metal remains the slight optimism since Wednesday. However, the revived dollar strength is weighing on the yellow metal, as it makes the Dollar a better safe-haven assets than the Golds. The RSI for Gold reads 54.75, showing that the demand for gold remains positive. The pair now lies above its 20, 50 and 200 DMAs.

Resistance: 1830, 1860

Support: 1800, 1785, 1765

Economic Data:

|

Currency

|

Data

|

Time (GMT + 8)

|

Forecast

|

|

CNY

|

GDP (YoY) (Q4)

|

10:00

|

3.6%

|

|

CNY

|

Industrial Production (YoY) (Dec)

|

10:00

|

3.6%

|

|

EUR

|

CPI (YoY) (Dec)

|

18:00

|

4.9%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|