In a mixed day for the financial markets, the Nasdaq Composite faced a 1.04% decline on Tuesday, spurred by Oracle’s sharp 13.5% drop following disappointing results. This decline, though not a massive stock, reflects broader business spending trends and impacted both the Nasdaq and the S&P 500. Meanwhile, tech giants like Apple and Adobe also saw their share prices decline. On the energy front, U.S. crude oil prices hit their highest level since last November, boosting energy stocks. In the currency market, the US Dollar Index showed a modest increase as investors awaited the release of the August US Consumer Price Index (CPI), which is expected to influence Federal Reserve monetary policy expectations. The week also holds key inflation data with the Producer Price Index (PPI) scheduled for Thursday. In the UK, mixed labor market data pointed to economic challenges, while in currency trading, the Pound weakened amid uncertainties. The EUR/USD pair faces upcoming Eurozone Industrial Production data and the European Central Bank’s meeting.

Stock Market Updates

On Tuesday, the Nasdaq Composite experienced a 1.04% decline, marking its first day of losses in three days. This drop was primarily driven by the sharp decline in Oracle shares, which tumbled 13.5% following disappointing quarterly results and a lackluster revenue forecast. This setback in Oracle, while not a massive stock, is indicative of larger business spending trends, impacting both the Nasdaq and the S&P 500. Additionally, other tech giants like Amazon, Alphabet (Google’s parent company), and Microsoft also saw their stock prices slide.

Meanwhile, Apple’s shares fell by 1.7% after the announcement of a new iPhone model, and Adobe’s shares dropped approximately 4% ahead of its upcoming earnings report. On a different note, U.S. crude oil prices reached their highest level since November of the previous year, driven by OPEC’s optimistic demand growth forecast. This surge in oil prices provided a boost to energy stocks, with Chevron and Exxon Mobil both seeing gains of about 1.9% and 2.9%, respectively. Investors are now closely watching key inflation data set to be released later this week, along with the European Central Bank’s interest rate decision on Thursday.

Investors eagerly await the release of key inflation data later this week, especially following a series of stronger-than-expected economic indicators from the previous week, which raised concerns about the possibility of the Federal Reserve increasing rates more than previously anticipated.

Data by Bloomberg

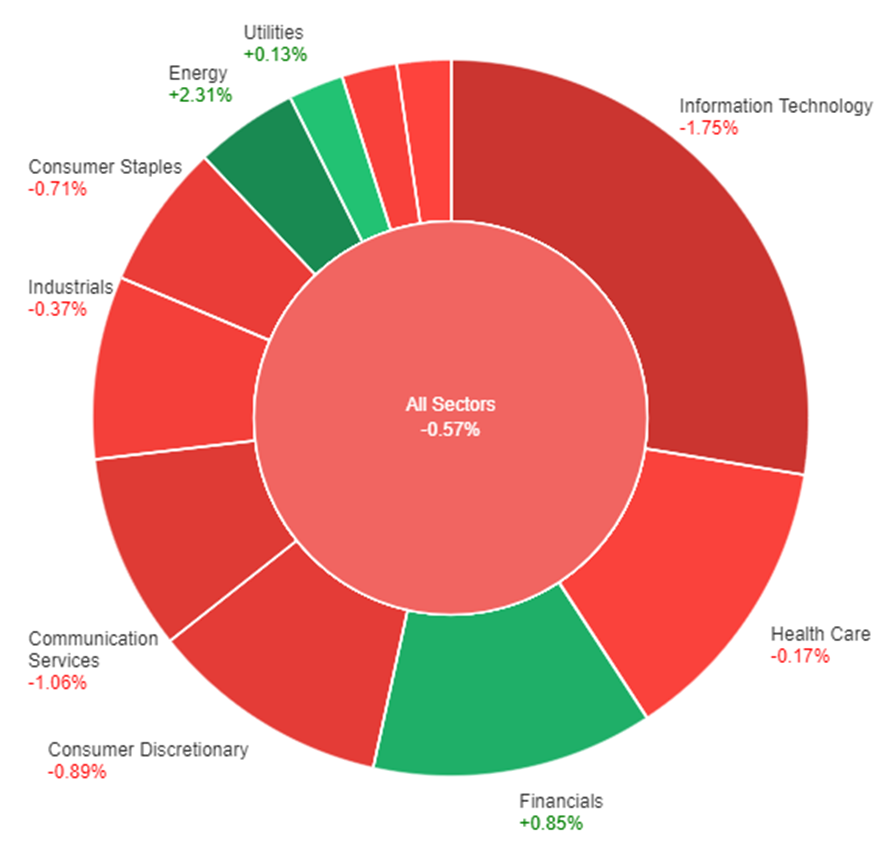

On Tuesday, the overall market slipped by 0.57%, with notable sector performance variations. Energy surged by 2.31%, and financials gained 0.85%, while utilities and real estate had slight gains of 0.13% and -0.03%, respectively. In contrast, information technology saw a substantial 1.75% drop, and communication services declined by 1.06%. Consumer discretionary, industrials, materials, and health care sectors faced moderate declines ranging from -0.17% to -0.89%, while consumer staples decreased by 0.71%. These sector-specific movements contributed to the market’s overall decline.

Currency Market Updates

The US Dollar Index saw a modest uptick on Tuesday, nearing 105.00 before retracing, with markets relatively calm as they awaited crucial US data. The highlight of the week, the August US Consumer Price Index (CPI), is scheduled for release on Wednesday. It’s expected to show an annual rate rebound from 3.2% to 3.6%, while the Core rate may slow down from 4.7% to 4.3%. These figures are poised to influence expectations about the Federal Reserve’s monetary policy, likely leading to increased volatility. Thursday will bring more inflation data with the Producer Price Index (PPI).

In the UK, mixed labor market data signaled a deteriorating economic situation, as the unemployment rate rose to 4.3% – the highest since September 2021 – accompanied by a decline in employment by 207K. Despite average hourly weekly earnings exceeding expectations at 8.5%, the Pound weakened. The GBP/USD pair approached its monthly low before rebounding toward 1.2500. Meanwhile, the EUR/USD pair reached a weekly high at 1.0769 and has Eurozone Industrial Production data scheduled for Wednesday, along with the European Central Bank’s Governing Council meeting on Thursday.

Picks of the Day Analysis

EUR/USD (4 Hours)

EUR/USD Sees Modest Pullback Ahead of Key Economic Data and ECB Meeting

The EUR/USD pair experienced a moderate pullback on Tuesday, initially spiking to 1.0769 during the Asian session, its highest level in a week, before retracing while still holding above the 1.0700 mark. Investors are eagerly awaiting the release of US consumer inflation data and the European Central Bank (ECB) meeting.

The market received mixed signals from Germany, with the current condition index dropping to -79.4, its lowest point since August 2020, and the expected index coming in at -11.4, surpassing the forecast of -15.0. These indicators contribute to concerns about a potential recession in Germany and the Eurozone, impacting expectations regarding an ECB rate hike. Market pricing suggests a nearly 50% probability of a rate hike on Thursday, but most analysts anticipate at least one 25 basis points rate hike by year-end. The economic outlook of the Eurozone, in contrast to the more resilient US economy, remains a critical factor influencing the direction of the EUR/USD pair, with the US Consumer Price Index (CPI) report on Wednesday poised to play a pivotal role in shaping market sentiment.

According to technical analysis, EUR/USD moved higher on Tuesday and is currently trading just below the upper band of the Bollinger Bands. This movement suggests the possibility of further continuation to the upside, potentially pushing towards the upper band. The Relative Strength Index (RSI) is currently at 57, indicating that EUR/USD is in a neutral stance with a slight bullish bias.

Resistance: 1.0759, 1.0803

Support: 1.0702, 1.0653

XAU/USD (4 Hours)

XAU/USD Dips Amid Dollar Demand but Recovers Slightly as Markets Await US CPI Data

Gold prices saw a decline on Tuesday, influenced by renewed demand for the US Dollar, as XAU/USD dropped to $1,907.53 per troy ounce. The decline in the precious metal was most pronounced during European trading hours, as weak local data raised concerns about economic setbacks in the United Kingdom and the Euro Zone.

However, the mood improved as Wall Street opened, with local indexes outperforming their international counterparts. The Dow Jones Industrial Average was in positive territory, while the S&P500 and the Nasdaq Composite posted minor losses. XAU/USD managed to recover some of its earlier losses, trading at approximately $1,912 per troy ounce.

Speculative traders are exercising caution in anticipation of significant events scheduled for the latter part of the week, refraining from making strong commitments. Nevertheless, Gold has been among the weakest performers against the US Dollar this week. Attention now turns to the United States (US) Consumer Price Index (CPI), which is expected to rise by 0.6% MoM and 3.6% YoY, surpassing July’s figures. Higher-than-expected CPI numbers could fuel speculation about an impending Federal Reserve (Fed) rate hike, benefiting the USD in a risk-averse environment. Conversely, if CPI figures fall short of market expectations, markets may turn notably optimistic.

According to technical analysis, XAU/USD moved lower on Tuesday and reached the lower band of the Bollinger Bands. Currently, the price is trading slightly above the lower band with the potential for further downward movement. The Relative Strength Index (RSI) is currently at 35, indicating that the XAU/USD pair is still biased towards the bearish side.

Resistance: $1,919, $1,925

Support: $1,910, $1,903

Economic Data

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| GBP | GDP m/m | 14:00 | -0.2% |

| USD | Core CPI m/m | 20:30 | 0.2% |

| USD | CPI m/m | 20:30 | 0.6% |

| USD | CPI y/y | 20:30 | 3.6% |