거래거래

학원학원

홍보홍보

회사회사

VT와 파트너 관계를 맺다VT와 파트너 관계를 맺다

On Wednesday, the stock market exhibited a blend of movements as the S&P 500 set a new record high, driven by a technology stock rally led by Netflix. While the S&P 500 and Nasdaq Composite saw positive gains, the Dow Jones Industrial Average faced a slight decline due to notable drops in Verizon and 3M following earnings reports. Netflix’s remarkable 10% surge, supported by an all-time high subscriber count, contributed to the broader tech sector’s strength in 2024. Microsoft and Meta also made significant gains, pushing the S&P 500 to record levels and confirming a new bull market. However, not all companies shared in the positive momentum, with AT&T and DuPont De Nemours facing setbacks. In the currency market, the dollar index declined, influenced by China’s stimulus measures, impacting pairs like USD/JPY and EUR/USD. The article concludes with a look ahead at upcoming economic data releases, central bank meetings, and geopolitical factors influencing the dynamic currency market.

The stock market experienced mixed movements on Wednesday, with the S&P 500 reaching a new record high, driven by a rally in technology stocks led by Netflix. The S&P 500 edged up 0.08% to close at 4,868.55, establishing a fresh all-time closing record, while the Nasdaq Composite gained 0.36%, marking the fifth consecutive day of positive performance for both indices. However, the Dow Jones Industrial Average slipped 0.26% to 37,806.39, impacted by notable declines in Verizon and 3M following their earnings reports. Netflix saw a significant surge of over 10% after announcing an all-time high subscriber count of 260.8 million and surpassing analysts’ revenue estimates, contributing to the broader tech sector’s strong performance in 2024.

In addition to Netflix’s positive impact, Microsoft’s shares rose nearly 1%, briefly pushing its market value above $3 trillion for the first time, while Meta advanced 1.4%, surpassing a $1 trillion market cap. These gains, along with the strong performance of communication services and information technology stocks, propelled the S&P 500 to record highs and confirmed a new bull market. However, not all companies shared in the positive momentum, with AT&T slipping about 3% due to lower-than-expected earnings, and DuPont De Nemours tumbling 14% after preannouncing weak fourth-quarter results and issuing disappointing first-quarter guidance. Traders continued to focus on earnings reports, with Tesla, Las Vegas Sands, and IBM scheduled to release results after the market close. As of the current earnings season, more than 71% of S&P 500 companies that have reported quarterly financials have exceeded Wall Street expectations, according to FactSet.

Data by Bloomberg

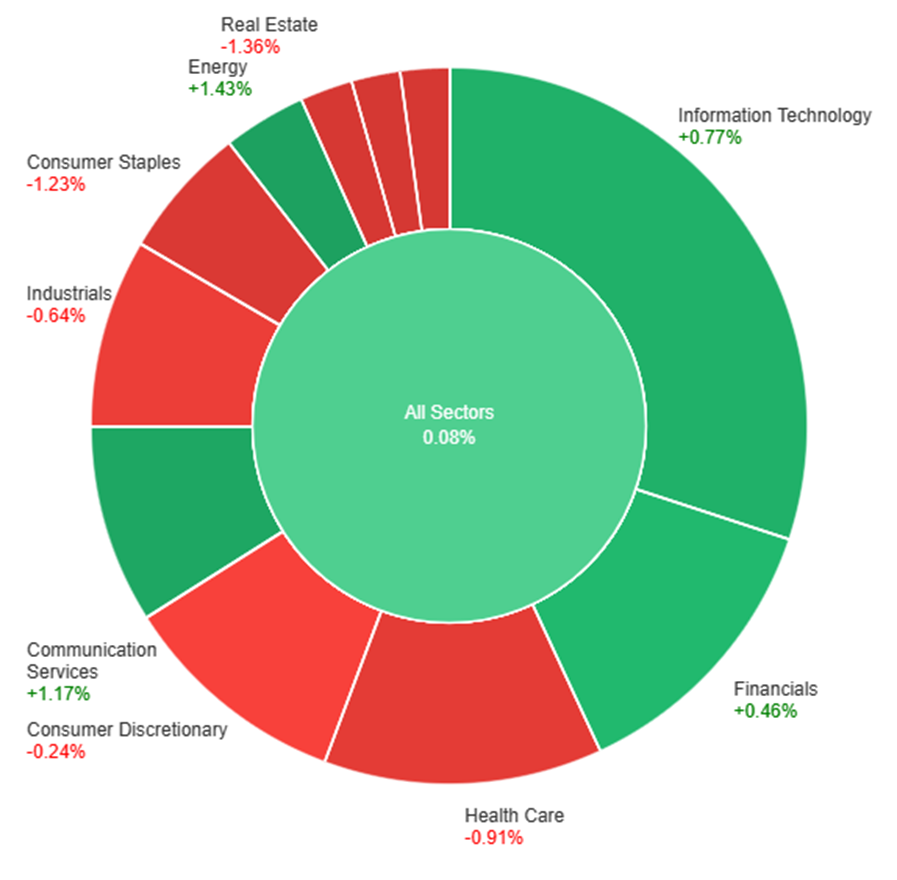

On Wednesday, the overall market saw a marginal increase of 0.08%. Notable positive performances were observed in the Energy sector, which gained 1.43%, followed by Communication Services at 1.17%, and Information Technology at 0.77%. Conversely, the

Consumer Staples, Real Estate, Utilities, and Materials sectors experienced declines of -1.23%, -1.36%, -1.38%, and -1.40%, respectively. The Consumer Discretionary sector also saw a modest decrease of -0.24%. Sectors such as Industrials and Health Care reported larger declines of -0.64% and -0.91%, respectively.

In the currency market updates, the dollar index experienced a 0.45% decline, driven by risk-on sentiments influenced by China’s stimulus measures. The USD/JPY pair saw a significant drop due to rising Japanese Government Bond (JGB) yields in response to the Bank of Japan’s somewhat hawkish meeting earlier in the week. However, a rebound in U.S. flash Purchasing Managers’ Index (PMI) numbers contributed to lifting Treasury yields and helping the dollar recover from its lows. The EUR/USD pair rose by 0.38%, reaching a high of 1.0930 before the U.S. PMI release. The positive impact of the U.S. manufacturing and service sector readings beating forecasts was tempered by a cooling price received index.

Looking ahead, attention in the currency market is shifting to upcoming hard U.S. data ahead of the Federal Reserve meeting next week. Key events include Q4 GDP and jobless claims on Thursday, followed by core Personal Consumption Expenditures (PCE), income, and spending on Friday. Additionally, post-European Central Bank (ECB) meeting events on Thursday may provide hints regarding the timing of the first rate cut, which is currently favored for April. Tokyo CPI data on Friday will also be closely monitored amid speculation about a Bank of Japan rate hike, with April’s BoJ meeting seen as the earliest potential venue for such a move. The article also notes the market’s modest preference for a March Fed rate cut in futures. Overall, the currency market remains dynamic, responding to a combination of economic data releases, central bank meetings, and geopolitical developments.

EUR/USD Surges as Intense Greenback Sell-Off and Positive Economic Indicators Overpower Rate Cut Speculations

In a surprising turn of events, the intense sell-off in the greenback allowed EUR/USD to overcome recent weaknesses, pushing past the 1.0900 hurdle and reaching new multi-day highs. The USD Index (DXY) faced headwinds in the risk-friendly environment, dropping below 103.00 despite an uptick in US yields. Speculation shifted away from a Fed rate cut in March, favoring a reduction in May. Contributing to the Euro’s strength were robust PMIs in Germany and the eurozone for January, suggesting a potential soft landing for the regional economy. As the ECB event approaches, market participants are weighing in on potential rate cuts, with debates arising on the timing of the central bank’s decision, further fueled by President Lagarde’s hints at a move during the summer.

On Wednesday, the EUR/USD moved higher, able to reach the upper band of the Bollinger Bands. Currently, the price is moving back lower to reach below the middle band, suggesting a potential downward movement to reach the lower band. Notably, the Relative Strength Index (RSI) maintains its position at 47, signaling a neutral outlook for this currency pair.

Resistance: 1.0890, 1.0954

Support: 1.0814, 1.0745

US Dollar Strengthens as Upbeat Data Pushes Gold (XAU/USD) to Weekly Low

In the American session, the US Dollar gained momentum, driving Gold (XAU/USD) down to $2,011.72, marking a fresh weekly low. The surge was fueled by optimistic US economic data, particularly the January Producer Manager Indexes (PMIs) released by S&P Global. Manufacturing output improved to 50.3, surpassing the previous 47.9 and reaching the highest reading in over a year. The Services PMI also exceeded expectations at 52.9, indicating the sharpest business activity growth in seven months. While the Bank of Canada (BoC) left its key rate unchanged at 5%, the statement was slightly more hawkish, reducing the likelihood of an April rate cut. Despite this, stock markets maintained a positive tone, with Wall Street resuming its record rally on better-than-anticipated earnings reports, signaling overall economic health.

On Wednesday, XAU/USD moved lower and was able to reach the lower band of the Bollinger Bands. Currently, the price moving around the lower band suggesting a potential upward movement to reach the middle band. The Relative Strength Index (RSI) stands at 43, signaling a neutral outlook for this pair.

Resistance: $2,035, $2,052

Support: $2,010, $1,993

| Currency | Data | Time (GMT + 8) | Forecast |

|---|---|---|---|

| EUR | Main Refinancing Rate | 21:15 | 4.50% |

| EUR | Monetary Policy Statement | 21:15 | |

| USD | Advance GDP q/q | 21:30 | 2.0% |

| USD | Unemployment Claims | 21:30 | 199K |

| EUR | ECB Press Conference | 21:45 |