Midweek, on Wednesday, 18 December 2024, the market is focusing on central bank policies, particularly the Federal Reserve’s decisions, and their implications for currency valuations. Additionally, movements in commodity-linked currencies and cryptocurrencies are contributing to a complex trading environment.

KEY INDICATORS

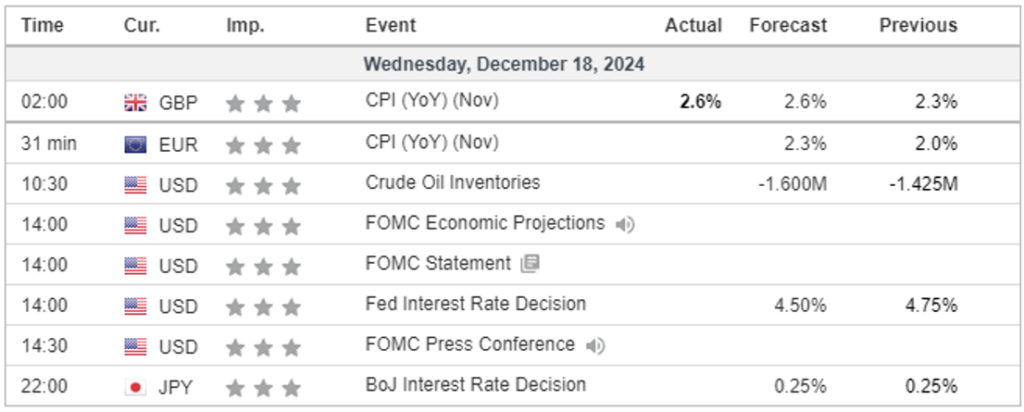

Federal Reserve meeting

- The US Federal Reserve is anticipated to announce a 0.25% rate cut today, marking its third consecutive reduction. Traders are closely monitoring the Fed’s updated projections for 2025, as any deviation from expectations could significantly impact the US dollar and global currency markets.

Bank of Japan

- The Bank of Japan (BoJ) is expected to maintain its current interest rates at the upcoming meeting, opting to assess international risks and the wage outlook for 2025 before making any policy changes. This cautious stance suggests that any rate hikes may be deferred to early 2025.

Commodity currencies and Chinese market influence

- Currencies such as the Australian dollar (AUD), Canadian dollar (CAD), and New Zealand dollar (NZD) are experiencing downward pressure, partly due to declining Chinese bond yields. These currencies are closely linked to China’s economic performance, and shifts in Chinese financial markets are affecting their valuations.

Cryptocurrency movements

- Bitcoin recently surpassed USD 108,000, achieving a new all-time high, before undergoing a significant reversal. This volatility underscores the dynamic nature of cryptocurrency markets, which continue to attract trader interest.

MARKET MOVERS

EUR/USD

A move toward 1.0525 would complete an intraday bearish Gartley pattern.

Economic data releases may negatively impact the short-term technical outlook.

There are no definitive signs that the current upward trend is nearing its conclusion.

Further upside potential is anticipated, and we aim to establish long positions in the early trading session.

Trade opportunity: Target 1: 1.0525 // Target 2: 1.06 // Expires: 19 December 2024

GER40 DAX

Price action suggests the formation of a potential top.

Daily sentiment indicators are showing overbought extremes.

Bearish divergence is anticipated to limit further gains.

Early optimism may drive initial gains but attempts to push higher are likely to face resistance and fail.

An Evening Doji Star formation has appeared at the recent high.

Trade opportunity: Target 1: 20105 // Target 2: 20005 // Expires: 19 December 2024

XAU/USD

Support is established at 2620 and is expected to limit any pullbacks to this level.

Initial pessimism may trigger losses, but sustained moves lower are unlikely to succeed.

Buying on dips presents a favorable risk/reward opportunity.

Levels below 2620 continue to draw strong buying interest.

Trade opportunity: Target 1: 2675.2 // Target 2: 2685.2// Expires: 19 December 2024

TODAY’S NEWS HEADLINES

US dollar strengthens as major currencies show mixed movements

- The US dollar strengthened against major currencies, with the dollar index rising to 106.97.

- EUR/USD declined by 21 pips to 1.0489 as Germany’s Ifo business climate index dropped to 84.7 in December (below the 85.3 forecast and 85.7 in November), while the ZEW economic sentiment index improved to 15.7 (beating the 6.9 forecast and up from 7.4 in November).

- USD/JPY fell by 62 pips to 153.53, halting a six-session winning streak.

- GBP/USD gained 25 pips to reach 1.2706, with the UK’s unemployment rate holding steady at 4.3%, in line with expectations.

- AUD/USD lost 36 pips, settling at 0.6334.

- USD/CHF edged down 16 pips to 0.8924.

- USD/CAD rose by 69 pips to 1.4311, as Canada’s annual inflation rate slowed to 1.9% in November (below the 2.1% estimate and October’s 2.0%).

US stocks fall ahead of Fed decision

- On Tuesday, US stocks declined ahead of the Federal Reserve’s interest rate decision. The Dow Jones Industrial Average lost 267 points (-0.61%) to close at 43,449, marking its ninth consecutive loss—the longest streak since 1978.

- The S&P 500 fell 23 points (-0.39%) to 6,050, while the Nasdaq 100 dropped 95 points (-0.43%) to 22,001. The yield on the US 10-year Treasury slipped one basis point to 4.385%.

- In economic updates, US retail sales rose 0.7% month-over-month in November (exceeding the +0.5% forecast and October’s +0.4% gain), while industrial production dipped 0.1% (below the +0.2% expected but an improvement from October’s -0.3%).

- European markets showed mixed results: the DAX 40 declined 0.33%, the FTSE 100 fell 0.81%, and the CAC 40 edged up 0.12%.

- US WTI crude oil futures dropped for the second straight session, losing USD 1.06 (-1.50%) to settle at USD 69.65 per barrel.

- Gold prices also declined, falling USD 6 to USD 2,646 an ounce.

Fed rate cut expected as US housing and UK inflation rise

- The US Federal Reserve is anticipated to lower interest rates by 25 basis points.

- In the US housing market, November housing starts are projected to grow by 2.3% month-over-month, while building permits are expected to increase by 1.3%.

- The UK’s annual inflation rate for November is forecast to edge up to 2.6%.

Click here to open account and start trading.